The swift increase in home prices might decelerate, yet the limited supply will continue to create demand pressures.

Even with expectations that increasing mortgage rates will temper the competitive real estate market, housing supply and listing prices are unlikely to revert to pre-pandemic levels in the near future.

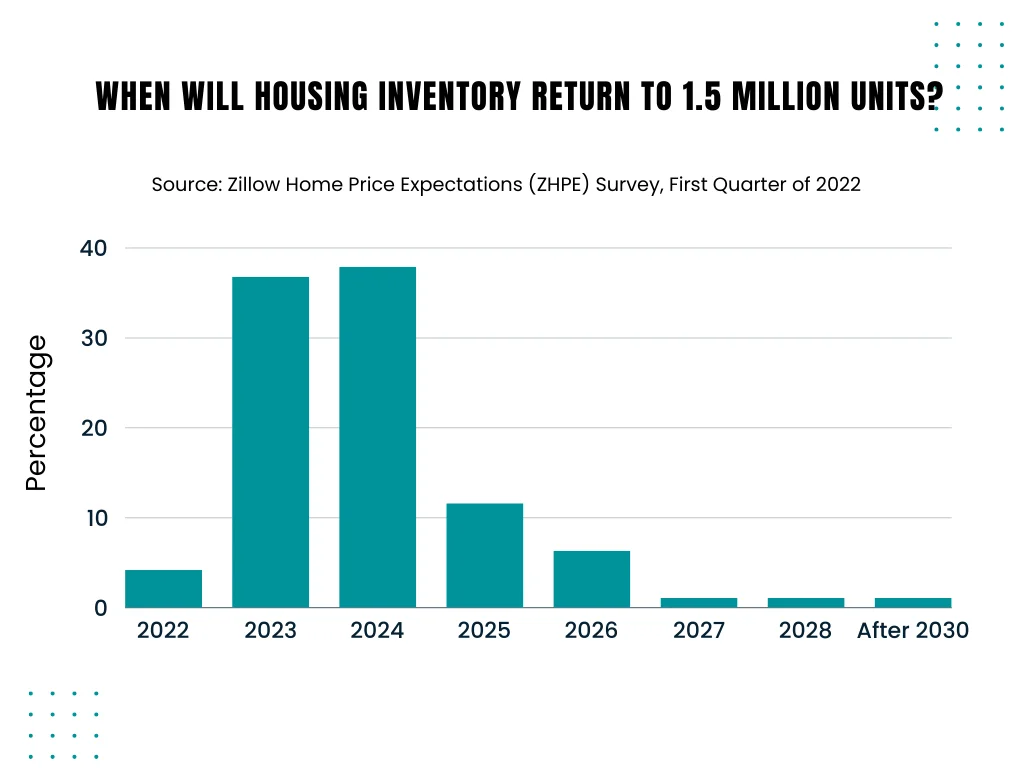

According to the latest Zillow Home Price Expectations Survey (ZPHE), real estate experts anticipate that housing inventory won’t reach a monthly average of at least 1.5 million available units until the end of 2024. Economists also concur that while home price appreciation will decelerate, it will persist in its growth trajectory over the coming years.

“As we move into the busiest selling season of the year, we’re observing new listings reappearing in the market at a gradual pace. However, it will take a considerable amount of time to address this shortage in supply,” commented Zillow Senior Economist Jeff Tucker.

Continue reading to delve into Zillow’s updated housing market forecast. If you’re contemplating purchasing a home or refinancing your mortgage this year, you can visit Credible to compare interest rates at no cost, without affecting your credit score.

While the Rate of Home Price Appreciation Might Decrease, Annual Increases are Expected to Remain Substantial

In 2021, home prices appreciated by 19% due to limited supply and robust demand from buyers taking advantage of low mortgage rates. Although rising interest rates could dampen demand, Zillow’s surveyed experts anticipate median prices to still rise by 9% in 2022 as inventory remains constrained.

On average, survey participants project a 26.8% increase in home prices over the next five years. The most optimistic respondents foresee a 46.5% increase by the end of 2026, whereas more conservative estimates suggest a 10.3% appreciation rate during that period.

While this may appear daunting for newcomers to the housing market, the optimistic long-term growth projection provides a ray of hope for determined individuals looking to purchase a home in today’s fiercely competitive environment.

“Inventory levels and mortgage rates will play a crucial role in determining the extent and pace of home price increases this year and in the future,” remarked Tucker.

If you’re contemplating buying a home amid rising mortgage rates, it’s essential to explore options from various lenders. You can utilize Credible to compare mortgage rates and secure the most favorable rate tailored to your financial circumstances.

Existing Homeowners could See Advantages from a Rise in Home Equity

Homebuyers aren’t the only ones who should take notice of the surge in home values. Existing homeowners may want to consider leveraging their substantial home equity through a cash-out mortgage refinance.

Cash-out refinancing involves obtaining a larger mortgage than your current outstanding balance, receiving the excess amount in cash. This option can enable homeowners to pay off high-interest debts or fund home improvement projects at a lower interest rate compared to unsecured personal loans.

Keep in mind that refinancing a home loan incurs closing costs, typically ranging from 2% to 5% of the total loan amount. Additionally, it’s essential to ensure that you can secure a competitive mortgage rate compared to your current rate.

Despite the upward trend in mortgage interest rates, some homeowners may still find refinancing advantageous. You can review the current mortgage rates provided in the table below to assess the feasibility of refinancing. Moreover, consulting with a knowledgeable loan expert at Credible can help determine if mortgage refinancing aligns with your financial goals.

Further reading: What is 40 Year Mortgage and How to Find It?

What Affects Home Price Growth Rate?

Several factors can influence the growth rate of home prices. These factors can be broadly categorized into economic, demographic, and geographic factors. Here are some key factors that can affect the growth rate of home prices:

- Economic Conditions: The overall health of the economy plays a significant role. Factors such as employment rates, wage growth, inflation, interest rates, and the state of the housing market (supply and demand dynamics, housing inventory levels, affordability) can all impact home price growth.

- Demand and Supply: The balance between supply and demand for homes in a particular area is crucial. If there’s high demand but limited supply, home prices tend to rise. Conversely, an oversupply of homes relative to demand can lead to slower price growth or even price declines.

- Interest Rates: Mortgage interest rates directly affect the affordability of homes. Lower interest rates can stimulate demand as they make mortgages more affordable, leading to potential price increases. Conversely, higher interest rates can dampen demand and slow down price growth.

- Local Market Conditions: Each housing market is unique, and factors such as job growth, local economic conditions, infrastructure development, and amenities can impact the demand for housing and consequently influence price growth.

- Demographics: Population growth, changes in household formation (such as more millennials entering the housing market), and migration patterns can all affect the demand for housing and thus impact price growth.

- Government Policies: Government policies and regulations related to housing, zoning laws, tax incentives (such as first-time homebuyer programs or property tax rates), and lending practices can influence both demand and supply in the housing market.

- Consumer Confidence: Sentiment and confidence among homebuyers and investors can influence buying decisions. Positive consumer sentiment may lead to increased demand and higher prices, while negative sentiment can have the opposite effect.

- Market Speculation: Speculative activity in the housing market, such as flipping homes or investors buying properties for resale, can contribute to price volatility and impact overall price growth rates.

- Natural Disasters and Environmental Factors: Events like natural disasters, climate change impacts, or environmental regulations can affect property values, especially in areas prone to such risks.

- Global Factors: Global economic trends, geopolitical events, and international investment flows can also indirectly impact home price growth rates, especially in markets that are sensitive to global economic conditions or foreign investment.

It’s important to note that these factors can interact in complex ways, and the relative importance of each factor can vary depending on the specific location and timing within the housing market cycle.