To the disappointment of prospective homebuyers, property prices persist in their upward trajectory. Despite encountering some of the highest mortgage rates seen in the last two decades, there appears to be no halting the relentless rise in home prices.

The National Association of Realtors (NAR) reported another increase in prices for March, indicating a 4.8% uptick in median existing-home prices compared to last year, marking the ninth consecutive month of year-over-year increases. Similarly, the S&P CoreLogic Case-Shiller home price index for February registered a 6.4% rise from the previous year, further illustrating the sustained growth in housing prices.

Any hopes that the post-pandemic “housing recession” might alleviate some of the significant price surges in homes have been dashed. Initially, the U.S. housing market had shown signs of slowing down in late 2022, hinting at a potential correction in home prices. However, contrary to expectations, home values resumed their upward trend, dispelling notions of a looming housing market crash.

What the Data is Revealing

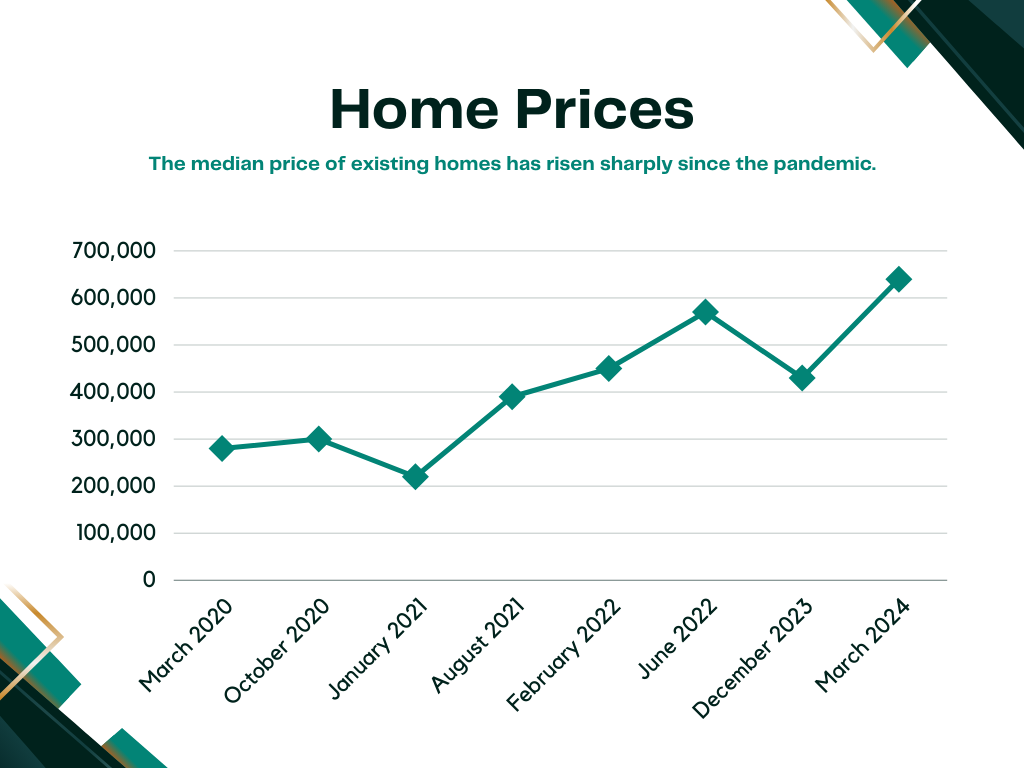

NAR data indicates that the median sale prices of existing homes are approaching record levels. In March 2024, the median price of $393,500 fell short of the all-time high of $413,800, but it still stands as the highest median for March on record. (Historically, late spring sees the highest prices due to seasonal fluctuations, with the all-time high being recorded in June 2022.)

The rapid increase in home prices compared to wages has created significant affordability challenges, according to Lawrence Yun, NAR’s chief economist. “Whenever home prices outpace people’s incomes, it raises concerns,” Yun recently informed reporters. This situation particularly impacts first-time buyers, while repeat buyers can leverage gains from the housing market and their investment portfolios for purchases.

Despite mortgage rates skyrocketing to 8% in October 2023 — reaching their highest levels in over 23 years — home values remained stable. (They have since decreased, briefly dipping below 7% before settling at an average of 7.39% in Bankrate’s weekly survey released on May 1.) The primary cause is a shortage of housing supply, with NAR’s March data indicating only a 3.2-month supply.

What Experts are Saying

Rick Arvielo, head of mortgage firm New American Funding, asserts, “We’re not going to see a decline in house prices. There simply isn’t enough inventory.” Skylar Olsen, chief economist at Zillow, concurs on the supply-demand disparity, forecasting further increases in home prices throughout 2024 — good news for sellers but challenging for first-time buyers aiming to enter the market.

In fact, the trend is moving in the opposite direction. According to Realtor.com’s April 2024 Housing Market Trends Report, the high mortgage rates have increased the monthly financing costs (after a 20% down payment) for the typical home by 6.9% since last year. This translates to about $148 more in monthly payments compared to April of the previous year — a substantial increase.

Considering these factors, housing economists and analysts anticipate any market corrections to be minor. No one anticipates price declines on the scale witnessed during the Great Recession.

Is an Impending Housing Market Crash Bound to Happen Soon?

Mark Fleming, the chief economist at title insurer First American Financial Corporation, emphasizes that the imbalance between buyers and sellers prevents a significant price drop: “The scarcity of supply is a fundamental issue,” he explains. “There are more buyers than available housing, a basic concept in economics.”

Dave Liniger, the founder of real estate brokerage RE/MAX, points out that the substantial increase in mortgage rates has disrupted the market. Many potential buyers have delayed purchases in anticipation of lower rates. However, a notable decline in mortgage rates could prompt a surge in new buyers, leading to higher home prices.

Liniger mentions, “There’s a whole generation of pent-up demand waiting to enter the market. We’re in an intriguing situation with high demand and limited inventory. When interest rates eventually decrease, we could see another cycle of rapid growth followed by a slowdown.”

While some previously active markets like Austin, Texas, have experienced minor price decreases, Lawrence Yun from NAR doesn’t foresee widespread price drops. He states, “Prices will stay strong and won’t decline nationally.”

Key Housing Market Statistics

- As per Bankrate’s weekly national survey of major lenders, the average interest rate for a 30-year mortgage loan stood at 7.39% as of May 1st.

- The National Association of Realtors reports a 4.3% decline in existing-home sales from February to March, with a further 3.7% drop compared to March 2023 to March 2024.

- According to NAR, the median sale price across the nation in March reached $393,500, marking an increase from both the prior month and the previous year, and setting a new record high for March.

- During March, the housing market possessed a 3.2-month supply of housing inventory, significantly lower than the 5 to 6 months typically required for a robust, balanced market that doesn’t favor either buyers or sellers.

- The most recent data from ATTOM Data Solutions indicates that 96,349 homes in the United States experienced foreclosure filings, including default notices, scheduled auctions, or bank repossessions, during the first quarter of this year. This reflects a 2.6% increase from the previous quarter but a 0.4% decrease from Q1 2023. Delaware stood out with the highest foreclosure rate among states during the winter months, with one foreclosure filing for every 894 housing units.

Between 2005 and 2007, the U.S. housing market appeared excessively inflated before it crashed, leading to catastrophic repercussions. The bursting of the real estate bubble triggered the most profound economic downturn since the Great Depression. Now, with the recent surge in mortgage rates and the looming possibility of a recession—Bankrate’s latest expert survey suggests a 33% chance—potential buyers and current homeowners are wondering when the housing market might experience another crash.

However, housing experts are in consensus that a crash is not imminent. While there could be a decline in prices, it’s unlikely to be as drastic as during the Great Recession. One significant difference between then and now is the stronger financial positions of homeowners today. The average homeowner with a mortgage boasts excellent credit, substantial home equity, and a fixed-rate mortgage secured at a low interest rate. In fact, an analysis by Realtor.com at the end of 2023 revealed that two-thirds of existing mortgages had rates below 4 percent.

Additionally, home builders vividly remember the challenges of the Great Recession and have been prudent in their approach to construction pace. Consequently, there remains a persistent shortage of homes available for sale. “The inventory shortage is a critical factor,” notes Yun. “While some markets might witness price decreases, the likelihood of a 30% price plunge repeating is extremely low.”

Existing Home Prices

For quite some time, economists have foreseen a slowdown in the housing market as home values start facing challenges due to their rapid growth. Following a year-over-year decline in February 2023, which was the first in over a decade, the median sale price of single-family homes has resumed its upward trajectory. According to NAR, there was a 4.8% annual increase in March, marking the ninth consecutive month of year-over-year growth.

In general, home prices have surged at a much faster rate than incomes. This affordability strain is further intensified by the fact that mortgage rates have more than doubled since August 2021.

Experts Say Prices to Hold Strong

Although the housing market is indeed slowing down, this deceleration doesn’t resemble typical real estate downturns. Despite elevated prices, the actual number of home sales has dropped significantly, and available inventories remain insufficient to meet demand. Homeowners who secured 3% mortgage rates a few years ago are opting not to sell—understandably so, given that current rates are more than double that figure—resulting in an even tighter supply of homes for sale. Consequently, the correction will be nothing like the drastic collapse of property prices seen during the Great Recession, when certain housing markets witnessed a 50% plummet in values.

Yun emphasized in a statement last fall, “We will not see a recurrence of the 2008–2012 housing market crash. There are no risky subprime mortgages that could implode, nor an excessive oversupply and overproduction of homes.”

Ken H. Johnson, a housing economist at Florida Atlantic University, notes that the housing market is experiencing conflicting pressures. “I believe we are entering a phase of relatively stable housing price performance nationwide as high mortgage rates exert downward pressure on prices, while strong demand from new households and limited inventory exert upward pressure,” he explains. “These opposing forces should, for the time being, offset each other.”

Discover more of our Blog here: Is It True That You Can Build Wealth in Real Estate Investing Easily?

5 Reasons There Will Be No Housing Market Crash

Housing economists highlight five compelling factors indicating that a crash is not on the immediate horizon.

- Inventories are still very low: In a balanced market, there is usually a housing inventory supply of 5 to 6 months. According to the National Association of Realtors, the supply of homes for sale in March was only 3.2 months. Interestingly, this represents an improvement from early 2022 when the supply was a mere 1.7 months. The persistent shortage of inventory clarifies why many buyers find themselves compelled to raise prices through bidding. Furthermore, this situation implies that the current supply-demand dynamics won’t permit a price crash in the foreseeable future.

- Builders didn’t build quickly enough to meet demand: Homebuilders significantly scaled back operations following the previous crash, and they never fully returned to the levels seen before 2007. As a result, they currently face challenges in acquiring land and obtaining regulatory approvals swiftly enough to meet the soaring demand. Despite their efforts to construct as much as possible, a repetition of the excessive building seen 15 years ago seems improbable. Greg McBride, Bankrate’s chief financial analyst, points out, “The primary reason for the price surge is heightened demand coupled with limited supply. As builders introduce more homes to the market, more homeowners opt to sell, and potential buyers find themselves priced out of the market. This gradual process will eventually restore equilibrium between supply and demand, although it won’t occur overnight.”

- Demographic trends are creating new buyers: Demand for homes is robust from multiple angles. Numerous Americans who were already homeowners concluded during the pandemic that they required larger accommodations, particularly with the increased prevalence of remote work. Millennials, a sizable cohort in their prime purchasing age, are actively seeking homeownership, while Hispanics, an expanding demographic, also exhibit a strong interest in owning homes.

- Lending standards remain strict: In 2007, “liar loans” were prevalent, allowing borrowers to obtain mortgages without documenting their income. Lenders were offering mortgages to almost anyone, regardless of their credit history or the size of their down payment. Nowadays, lenders have implemented stringent criteria for borrowers, and the majority of those securing mortgages boast excellent credit. According to the Federal Reserve Bank of New York, the median credit score for new mortgage borrowers in the fourth quarter of 2023 was an impressive 770. Greg McBride remarks, “If lending standards relax and we return to the lax days of 2004-2006, that presents a completely different scenario. If prices start rising due to the artificial purchasing power created by loose lending standards, then we should be concerned about a crash.” On the contrary, recent Federal Reserve data from a survey of senior loan officers indicates that lending standards have tightened even further, anticipating increased demand when interest rates eventually decline.

- Foreclosure activity is muted: Following the housing crash, numerous foreclosures inundated the housing market, causing prices to plummet. However, this is no longer the situation. Presently, the majority of homeowners possess substantial equity in their homes. During the peak of the pandemic, lenders refrained from filing default notices, leading to historically low foreclosure rates in 2020. Although there has been a slight increase in foreclosures since that time, it is nowhere near the levels seen previously.

All of that adds up to a consensus: Yes, home prices are still pushing the bounds of affordability. But no, this boom shouldn’t end in bust.