Interest rates wield significant influence over the housing market, often shaping the decisions of both homebuyers and sellers. They act as a pivotal factor in determining the affordability and accessibility of homeownership. In this article, we delve into the intricate relationship between interest rates and home acquisition power, exploring how fluctuations in interest rates can impact prospective buyers and the broader housing market dynamics.

In any real estate market, there’s invariably someone advocating, “Now is the ideal moment to buy (or sell)!” Yet, the notion of the “perfect time” is inherently subjective, contingent upon the individual circumstances of buyers or sellers. As someone who frequently discusses local market conditions, my aim is to remain impartial, present factual information, and refrain from adopting an overly persuasive approach with potential clients.

PITI, a prevalent term in the mortgage realm, represents Principal, Interest, Taxes, and Insurance, collectively constituting your entire mortgage payment. The interest component of PITI remains fixed throughout the loan term. For instance, if you secure a 30-year fixed-rate mortgage at 4%, that interest rate persists for the entire 30 years, unless you opt for early loan repayment, refinancing, or selling the property.

Below is a straightforward illustration showcasing the variations in your principal and interest payments across different interest rates for a 30-year fixed-rate loan of $100,000:

- 6% – Monthly payment of $600 – $215,838 total costs

- 7% – Monthly payment of $725 – $314,685 total costs

- 8% – Monthly payment of $853 – $412,264 total costs

While examining the Primary Mortgage Market Survey conducted by FRED St. Loius FED, it reveals that the average rate for a 30-year fixed-rate mortgage this week stands at 6.87%.

Now, let’s delve into the concept of purchasing power. Simply put, purchasing power refers to the extent of the home you can afford within your allocated budget. For most individuals, adhering to a specific budget is imperative. As interest rates climb, the purchasing power diminishes, resulting in a reduced capacity to afford a larger home.

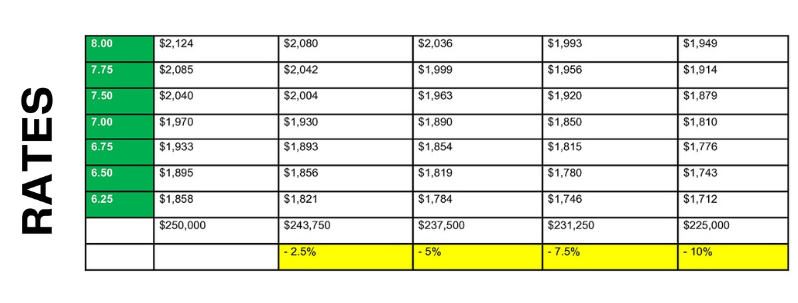

Outlined below are the potential impacts of varying interest rates on your monthly payments, with the aim of maintaining a principal and interest payment of approximately $1,100. This example is based on the national median sales price of $250,000.

In this scenario, for every quarter percentage point increase in your mortgage rate, the purchasing capacity for a home decreases by 2.5%.

While it may seem disheartening to hear about potential rate hikes after enjoying a period of favorable rates in recent years, it’s essential to recognize the numerous benefits of property ownership. Remember, even when rates stood at 6%, they were historically low at that time.

Other Things to Consider About Getting a Home Mortgage

- You’ll be eligible for a tax deduction on your mortgage interest

- Real estate taxes qualify for tax deductions

- Tax deductions can be claimed on Mortgage Insurance Premiums, if they are applicable

- Certainly, if you can make a cash payment, interest rates would have no impact on you whatsoever. Similarly, if you can provide a sizable down payment, your purchasing power would remain largely unaffected.

- What qualifies as a high rate? Keeping an eye on interest rates is crucial when considering a home purchase, but historically speaking, even rates of 5% or 6% are still considered quite favorable.

- Appreciation and depreciation—what are the prevailing market conditions in the area where you intend to purchase? Have home prices seen an upward trend over the past six months, year, or two years?

- Refinancing is an option to consider. While we, as non-experts, cannot accurately forecast future interest rates, purchasing at a higher rate allows for the possibility of refinancing if rates decline in the coming years. Although there are associated costs with refinancing, it could potentially be a financially prudent decision.

The Basics of Interest Rates

Interest rates, set by central banks, dictate the cost of borrowing money. They are essentially the price lenders charge borrowers for the use of their funds. These rates are influenced by various economic factors such as inflation, monetary policy, and overall market conditions. When interest rates rise, the cost of borrowing increases, making loans more expensive. Conversely, when interest rates fall, borrowing becomes cheaper.

Impact on Mortgage Rates and House Acquisition Power

Mortgage rates, which are influenced by prevailing interest rates, play a crucial role in determining the affordability of homeownership. Mortgage rates fluctuate in response to changes in the broader economy and monetary policy decisions. Higher interest rates lead to higher mortgage rates, making monthly mortgage payments more expensive. This can decrease the purchasing power of prospective homebuyers, as they may qualify for smaller loan amounts or find it challenging to afford monthly payments.

Affordability and Purchasing Power

Interest rates directly impact the affordability of homes by affecting the monthly mortgage payments. When interest rates are low, homeowners can secure lower mortgage rates, resulting in more affordable monthly payments. This can increase the purchasing power of buyers, allowing them to afford larger homes or more desirable properties. Conversely, higher interest rates can erode purchasing power, limiting options for potential buyers and potentially dampening demand in the housing market.

Impact on Housing Demand

Fluctuations in interest rates can significantly influence housing demand. Lower interest rates stimulate demand by making homeownership more affordable. Prospective buyers are incentivized to enter the market, leading to increased competition and potentially driving up home prices. Conversely, higher interest rates can suppress demand as affordability diminishes. This can lead to a slowdown in home sales and may exert downward pressure on prices.

Refinance Activity

Interest rate movements also impact refinance activity in the housing market. When interest rates decline, homeowners may have the opportunity to refinance their existing mortgages at lower rates, potentially reducing their monthly payments. This can free up additional funds for homeowners to spend or save, contributing to economic activity. Conversely, rising interest rates may deter homeowners from refinancing, limiting this avenue for potential savings.

Economic Indicators and Interest Rates

Interest rates are closely linked to broader economic indicators such as inflation, employment, and GDP growth. Central banks adjust interest rates in response to changes in these indicators to achieve specific economic objectives, such as controlling inflation or stimulating economic growth. Understanding the relationship between interest rates and economic fundamentals is essential for anticipating future interest rate movements and their potential impact on the housing market.

Recommended reading: Understanding the Ins and Outs of a Home Equity Line of Credit (HELOC)

Long-Term vs. Short-Term Impact

While short-term fluctuations in interest rates can have immediate effects on housing market dynamics, long-term trends also play a significant role. Long-term interest rate trends can influence buyer behavior, investment decisions, and overall market sentiment. For example, a prolonged period of low interest rates may fuel robust housing demand and price appreciation, while a sustained increase in rates could lead to a cooling of the market over time.

Considerations for Homebuyers

For prospective homebuyers, understanding the interplay between interest rates and home acquisition power is crucial for making informed decisions. Monitoring interest rate trends and economic indicators can provide valuable insights into the direction of the housing market. Additionally, considering factors such as personal financial circumstances, affordability, and long-term goals can help buyers navigate changing market conditions and secure favorable financing terms.

Conclusion

Interest rates exert a profound influence on the housing market, shaping the affordability, accessibility, and dynamics of homeownership. Fluctuations in interest rates can impact mortgage rates, affordability, housing demand, and overall market sentiment. By understanding the role of interest rates in home acquisition power, buyers can make informed decisions and adapt to changing market conditions effectively. Keeping abreast of interest rate trends and economic indicators is essential for navigating the complexities of the housing market and achieving successful outcomes in the pursuit of homeownership.