The wealth gap between homeowners and renters has long been a significant issue in many societies, particularly in the United States. This disparity is driven by various factors, including property appreciation, tax advantages, and the ability to build equity. Understanding the causes, consequences, and potential solutions to this gap is essential for addressing broader economic inequality.

Causes of the Wealth Gap

Building Equity

Homeownership is often viewed as a cornerstone of wealth accumulation. When homeowners make mortgage payments, a portion of those payments goes toward the principal balance of the loan, thereby increasing their equity in the property. Over time, as homeowners pay down their mortgages, they own a larger share of their home, which represents a significant asset.

Renters, conversely, do not have this opportunity to build equity. Monthly rent payments do not contribute to owning the property, meaning renters are not building a financial asset through their housing expenses. This fundamental difference in financial mechanisms is a primary driver of the wealth gap.

Property Appreciation

Real estate typically appreciates over time, meaning that the value of homes generally increases. Homeowners benefit from this appreciation, which can substantially increase their net worth. For instance, a home purchased for $200,000 might be worth $300,000 ten years later, representing a $100,000 gain in wealth for the homeowner.

Renters do not benefit from property appreciation. Even if the value of the property they live in increases, this gain accrues to the landlord, not the tenant. Consequently, renters miss out on this significant source of wealth generation.

Tax Benefits

Homeowners often enjoy several tax advantages that renters do not. In many countries, including the United States, mortgage interest and property taxes are deductible, which can reduce taxable income and result in significant tax savings. These savings can be used to invest further, save for retirement, or pay down debt, all of which contribute to greater financial stability and wealth accumulation.

Renters, on the other hand, do not receive comparable tax benefits, which further exacerbates the wealth gap.

Forced Savings Mechanism

Mortgage payments act as a form of forced savings. Each payment reduces the principal of the loan, effectively saving money by increasing the owner’s equity in the property. This mechanism helps homeowners build wealth over time, often without actively thinking about it.

Renters lack this forced savings mechanism. While they might choose to save and invest on their own, the absence of a structured savings plan like a mortgage means they might struggle more with consistent wealth accumulation.

Consequences of the Wealth Gap

Economic Inequality

The wealth gap between homeowners and renters contributes to broader economic inequality. Homeowners typically have higher net worths than renters, allowing them to afford better education, healthcare, and investment opportunities. This disparity can perpetuate a cycle of poverty and limit social mobility for renters.

Financial Security

Homeowners often enjoy greater financial security compared to renters. They have a valuable asset that can be leveraged in times of financial need, such as through home equity loans or reverse mortgages. This safety net is not available to renters, making them more vulnerable to economic downturns and unexpected expenses.

Intergenerational Wealth Transfer

Homeownership facilitates intergenerational wealth transfer. Homes can be passed down to heirs, providing them with a valuable asset and a stronger financial foundation. This transfer of wealth helps perpetuate economic advantages across generations.

Renters are less able to provide such a legacy for their descendants, contributing to the persistence of wealth disparities across generations.

Potential Solutions

Increasing Access to Homeownership

One of the most effective ways to address the wealth gap is to increase access to homeownership, particularly for low- and middle-income families. Policies that provide down payment assistance, lower interest rates, and affordable housing options can help more people transition from renting to owning.

Expanding Affordable Housing

Expanding the supply of affordable housing can help reduce the financial burden on renters and provide more opportunities for saving and investment. Policies that incentivize the construction of affordable housing units and provide subsidies for low-income renters can be effective.

Enhancing Financial Literacy

Improving financial literacy among renters can help them make better financial decisions, such as saving for a down payment or investing in other wealth-building assets. Educational programs focused on budgeting, saving, and investing can empower renters to improve their financial situations.

Reforming Tax Policies

Reforming tax policies to provide more benefits to renters could help reduce the wealth gap. For example, implementing tax credits for renters or allowing deductions for rent payments could provide financial relief and improve renters’ ability to save and invest.

Encouraging Rent-to-Own Programs

Rent-to-own programs offer a pathway to homeownership for renters who might not initially qualify for a mortgage. These programs allow renters to gradually build equity in a property, ultimately transitioning to full ownership.

Study Confirms that Homeowners' Wealth is 40 Times Higher than Renters

According to new NAR data, most homeowners have gained over $100,000 in equity over the past decade, but disparities among racial groups remain.

Property values have significantly increased along with home prices over the last decade, resulting in over $100,000 in equity for most homeowners and underscoring homeownership as a vital means of building household wealth.

Middle-income homeowners have experienced a 68% appreciation in their property values since 2012, amassing $122,100 in wealth, according to a new report from the National Association of REALTORS® presented at the 2023 REALTOR® Broker Summit. During the same period, low-income homeowners earning less than 80% of their area’s median income gained $98,900 in equity, while upper-income households earning more than 200% of their area’s median income accumulated $150,800 in equity. These findings are detailed in NAR’s report, “Wealth Gains by Income and Racial/Ethnic Group.”

“This analysis demonstrates how homeownership acts as a catalyst for wealth building across diverse populations,” says NAR Chief Economist Lawrence Yun. “A monthly mortgage payment often functions as a forced savings account, enabling homeowners to build a net worth approximately 40 times greater than that of renters.”

In addition to these wealth gains, homeowners experienced a 21% reduction in debt over the last decade, according to the report. Many homeowners refinanced their mortgages in recent years, securing interest rates below 4%. These lower monthly payments have enabled many to pay off an even greater portion of their mortgages, the report highlights.

Discover more interesting blog topics like this one: Home Equity 101: A Comprehensive Guide to Your Home’s Hidden Wealth

Equity Gains are Not Equal

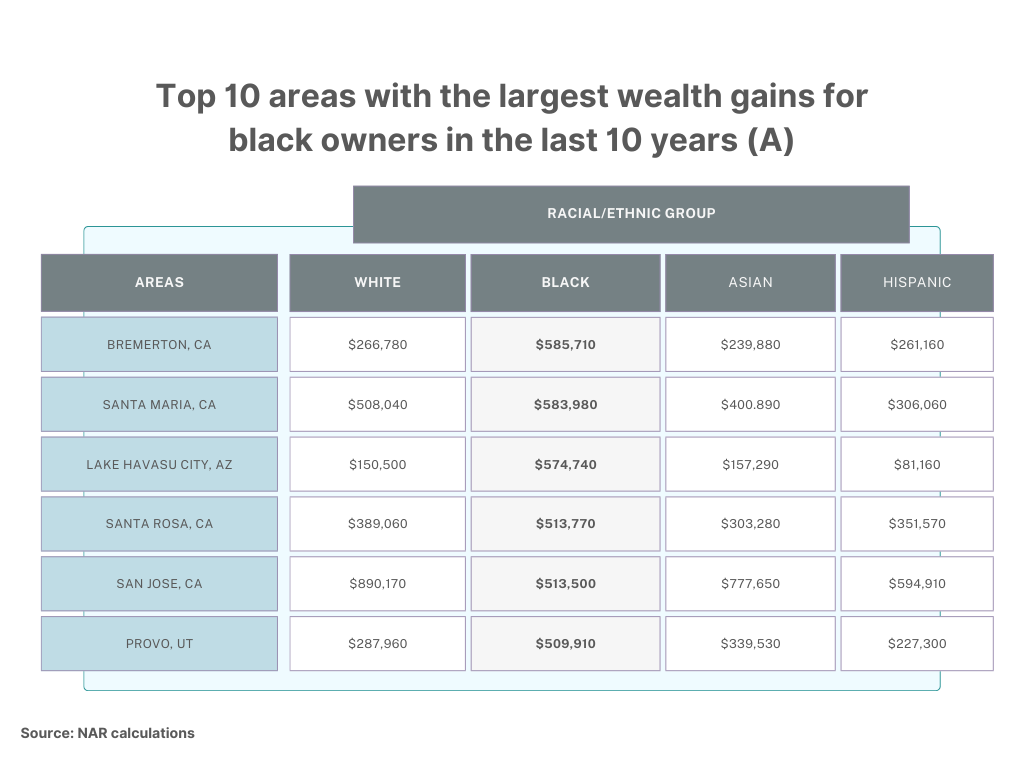

However, NAR’s report highlights the obstacles many Americans still encounter in accessing homeownership opportunities, noting “substantial variations and inequalities in homeownership rates across different incomes and racial and ethnic groups.” Black homeowners saw the smallest wealth gains over the past decade compared to other racial or ethnic groups, and Black homeownership rates remain notably lower.

“Data indicates that significantly fewer low-income households and households of color own their homes and have the opportunity to build wealth compared to other income and racial/ethnic groups,” the report states.

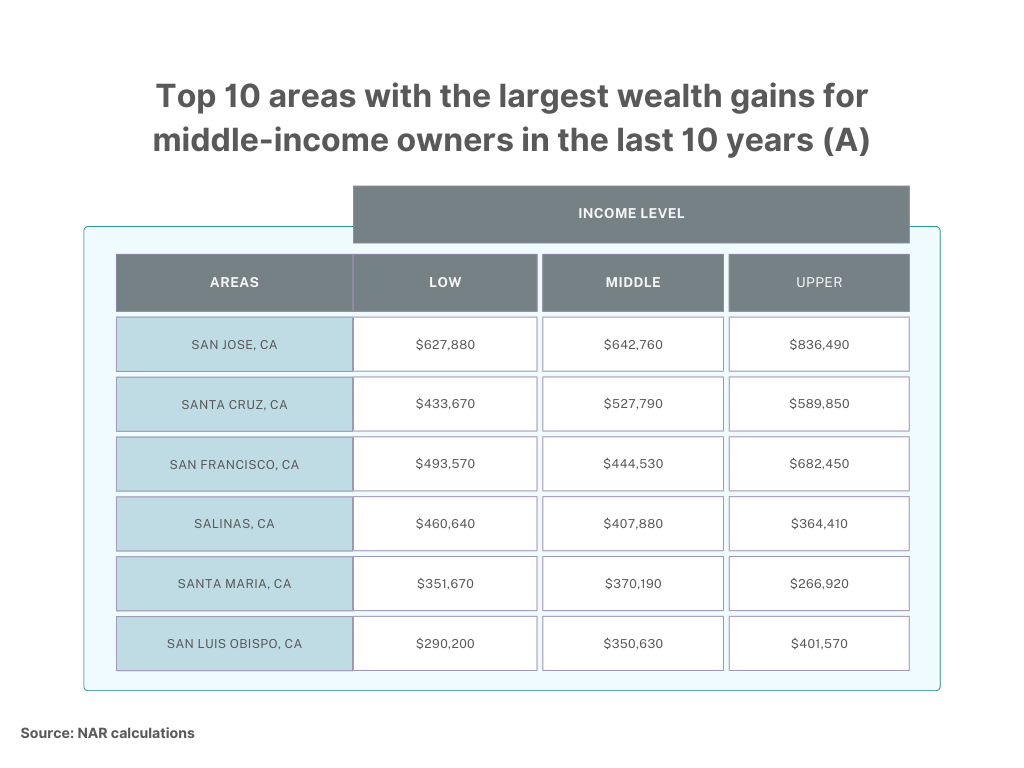

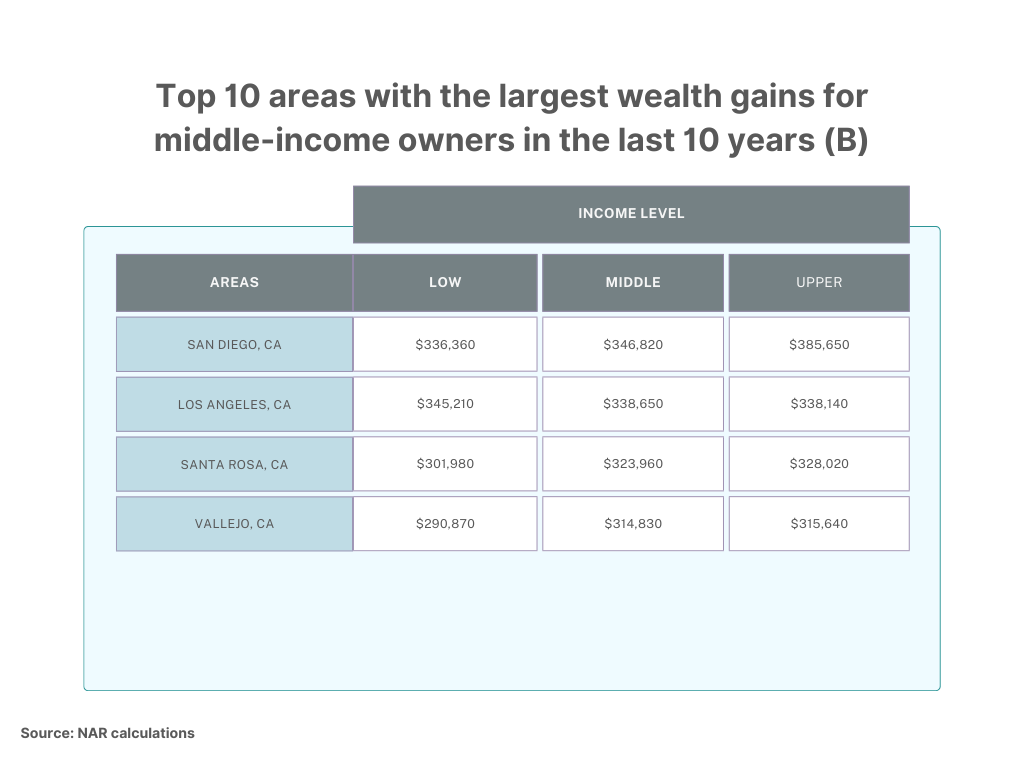

Largest Wealth Gains from Homeownership

Homeowners in expensive metro areas have experienced some of the most significant wealth gains over the past decade, according to NAR’s report. For instance, in the San Jose metro area, low-income earners accumulated nearly $630,000 in equity over the last 10 years, while middle-income earners gained $643,000. All of the top 10 areas with the largest wealth gains for low-income owners—with equity exceeding $290,000—are located in California.

The Bottom Line

The wealth gap between homeowners and renters is a multifaceted issue with deep-rooted causes and significant consequences. Homeownership offers distinct financial advantages, such as building equity, benefiting from property appreciation, and enjoying tax benefits, all of which contribute to greater wealth accumulation compared to renting.

Addressing this gap requires a comprehensive approach that includes increasing access to homeownership, expanding affordable housing, enhancing financial literacy, reforming tax policies, and encouraging innovative solutions like rent-to-own programs. By implementing these strategies, policymakers can help reduce economic inequality and provide more individuals with the opportunity to build wealth and achieve financial security.